How To Manage Debt as a Single Parent

Learning how to manage debt as a single parent can feel overwhelming, but with the right strategies and mindset, it’s completely achievable. Balancing job responsibilities with financial obligations requires planning, discipline, and smart decision-making. The good news is that even small, consistent actions can lead to significant progress over time.

In this guide, you’ll discover practical, easy-to-follow tips to help you take control of your finances without sacrificing your work performance or personal well-being.

Why Managing Debt Matters

Debt can quietly impact every part of your life—from stress levels to long-term financial goals. Whether it’s student loans, credit cards, or personal loans, unmanaged debt can grow quickly due to interest and missed payments.

When you actively work to manage debt, you:

- Reduce financial stress

- Improve your credit score

- Increase savings potential

- Gain more financial freedom

How To Reduce Your Debt: A practical guide explaining proven strategies like the snowball and avalanche methods, along with steps to organize and plan debt repayment.

Step 1: Understand Your Debt Situation

Before you can fix the problem, you need a clear picture of it.

Start by listing:

- Total debt amount

- Interest rates

- Minimum monthly payments

- Due dates

This step may feel uncomfortable, but it’s essential. Knowing exactly what you owe allows you to prioritize and build an effective repayment plan.

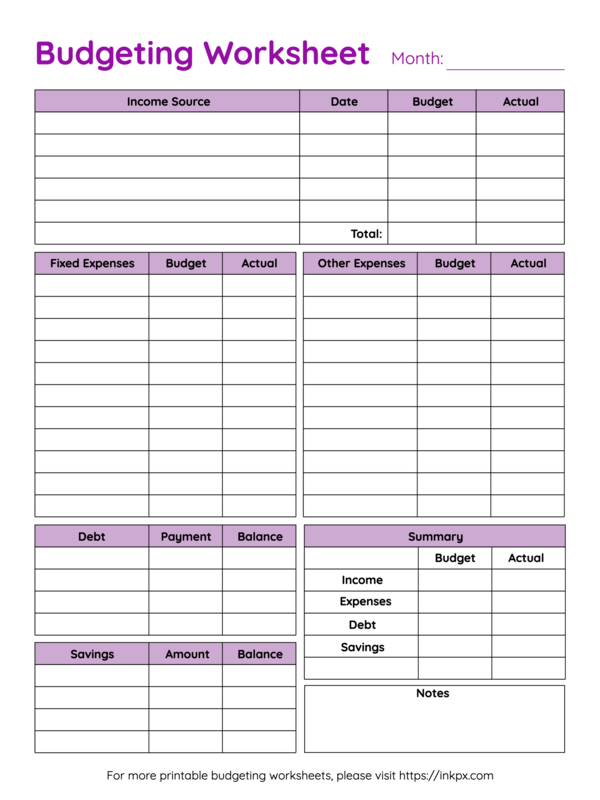

Step 2: Create a Realistic Budget

A budget is your foundation for financial success. When working full-time, your income is usually consistent—use that to your advantage.

Simple Budget Breakdown:

- 50% Needs (rent, utilities, groceries)

- 30% Wants (entertainment, dining out)

- 20% Debt repayment & savings

If your debt is high, consider adjusting this ratio to dedicate more toward repayment.

Tracking your spending helps you identify areas where you can cut back and redirect funds to manage debt more effectively.

Step 3: Choose a Debt Repayment Strategy

Not all repayment methods work for everyone. Choose one that matches your personality and financial situation.

– Debt Snowball Method

- Pay off smallest debts first

- Gain motivation from quick wins

– Debt Avalanche Method

- Focus on highest interest rates first

- Save more money in the long run

Both approaches are effective—it’s about consistency, not perfection.

Step 4: Automate Your Payments

When you’re working full-time, your schedule can get busy. Automating payments ensures you never miss a due date.

Benefits include:

- Avoiding late fees

- Protecting your credit score

- Reducing mental load

Set up automatic minimum payments and, if possible, schedule additional payments toward your principal.

Step 5: Cut Unnecessary Expenses

You don’t need to eliminate all fun, but small sacrifices can accelerate your progress.

Consider reducing:

- Subscription services

- Impulse purchases

- Frequent takeout meals

Redirect that extra money toward your debt. Even an additional $50–$100 per month can make a noticeable difference over time.

How To Get Out Of Debt: Covers budgeting, negotiating with creditors, and smart ways to regain control of your finances when dealing with debt.

Step 6: Increase Your Income Strategically

If your budget is tight, boosting your income can help you pay off debt faster.

Options include:

- Freelancing or side gigs

- Overtime hours

- Selling unused items

- Monetizing a skill or hobby

The key is to use any extra income specifically to manage debt, rather than increasing spending.

Step 7: Use Windfalls Wisely

Bonuses, tax refunds, or unexpected money can be powerful tools. Instead of spending it all:

- Allocate a large portion to debt repayment

- Keep a small amount for personal enjoyment

This balance keeps you motivated while still making progress.

Step 8: Build an Emergency Fund

It might seem counterintuitive, but saving while paying off debt is crucial.

Even a small emergency fund ($500–$1,000) can:

- Prevent new debt

- Cover unexpected expenses

- Reduce financial anxiety

Without it, one emergency could undo months of progress.

Step 9: Communicate with Creditors

If you’re struggling, don’t ignore the problem.

Many lenders offer:

- Lower interest rates

- Payment plans

- Temporary hardship programs

Being proactive can make it easier to stay on track.

Step 10: Stay Consistent and Patient

Debt repayment is a marathon, not a sprint. Progress may feel slow at times, but consistency is what delivers results.

Celebrate small wins:

- Paying off a credit card

- Reducing your balance

- Sticking to your budget for a month

These milestones build momentum and keep you motivated.

Common Mistakes to Avoid

While trying to manage debt, watch out for these pitfalls:

- Ignoring high-interest debt

- Taking on new unnecessary debt

- Not tracking spending

- Skipping payments

- Relying too heavily on credit

Avoiding these mistakes can save you time, money, and stress.

Work-Life Balance While Paying Off Debt

Managing debt doesn’t mean sacrificing your quality of life. Here’s how to maintain balance:

- Schedule time for relaxation

- Avoid burnout by setting realistic goals

- Reward yourself occasionally (within budget)

Remember, financial health and mental health go hand in hand.

Long-Term Financial Habits to Build

Once your debt is under control, focus on building sustainable habits:

- Regular saving

- Investing for the future

- Living below your means

- Tracking financial goals

These habits ensure you don’t fall back into debt and continue building wealth.

Final Thoughts

Learning how to manage debt as a single parent is one of the most valuable financial skills you can develop. It requires commitment, smart planning, and patience—but the rewards are worth it.

By taking control of your finances today, you’re creating a more secure and stress-free future.

Creating a budget is one of the most effective ways to stay on track financially. If you need help getting started, check out these Real-Life Budgeting Tips For Single Moms, which offer practical strategies you can apply immediately.

Explore our blog for more insights and helpful information.

Click here to learn more about our career and coaching services.

Have questions or feedback? Visit our Contact page (click here) — we’d love to hear from you.